If you’ve ever felt overwhelmed by the idea of budgeting, you’re not alone. Many people avoid it because it seems restrictive, time-consuming, or overly complicated. This practical blueprint simplifies the process and shows you exactly how to build a budget from scratch—without the stress. Using a clear, step-by-step framework inspired by proven financial principles and real-world wealth models, this zero based budgeting guide helps you assign every dollar a purpose and uncover immediate cost-saving opportunities. By the end, you’ll have a personalized budget in place and a focused plan to reduce expenses starting today.

Before you build wealth, you need clarity. The goal is simple: get an honest, data-driven picture of where your money is actually going, not where you think it’s going. For the next 30 days, track every single expense. Coffee, subscriptions, parking meters—nothing is too small.

At first, this feels tedious. However, the detail is the feature, not the flaw. Specific data reveals spending patterns, impulse triggers, and cash leaks that vague estimates hide.

You have three practical tools:

- Budgeting Apps: These automate transaction imports, categorize purchases in real time, and generate visual reports. The benefit? Speed and accuracy with minimal effort.

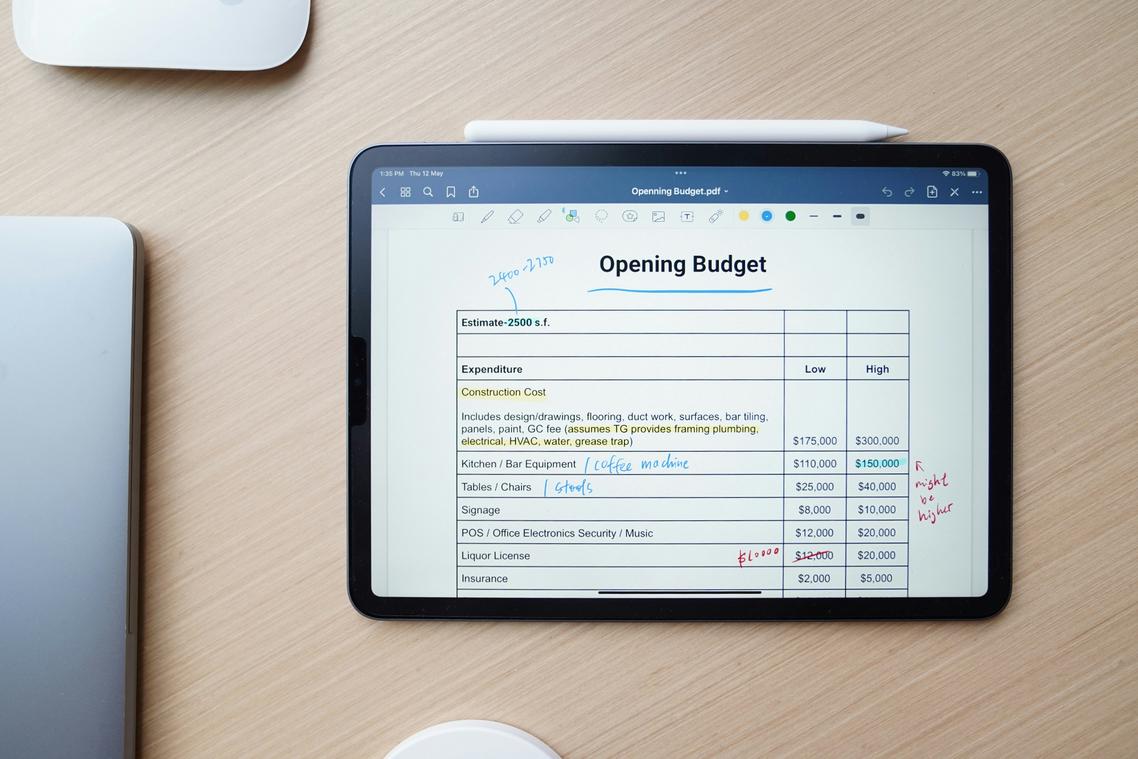

- The Simple Spreadsheet: Fully customizable columns, formulas, and monthly comparisons give you control and transparency.

- The Notebook Method: Writing expenses by hand increases awareness and reduces mindless spending.

Meanwhile, pair your tracking with a zero based budgeting guide to assign every dollar a job before the month begins.

Some argue tracking is restrictive or obsessive. In reality, it’s diagnostic. You can’t optimize what you don’t measure. After 30 days, you’ll see clear numbers, smarter choices, and opportunities to redirect money toward goals that actually matter.

Clarity today builds confidence and control for tomorrow. Start now. Seriously.

Step 2: Categorize and Confront – From Raw Data to Real Insights

By implementing a zero-based budgeting approach, you can take control of your finances and optimize your spending, much like the strategies discussed in our article on how Ocvibum Wealth makes money – for more details, check out our How Do Ocvibum Wealth Make Money.

Now that you’ve gathered your raw numbers, it’s time to organize them into categories that actually mean something. Data alone doesn’t change behavior—clarity does.

Start with three core buckets:

- Fixed Costs: Rent or mortgage, loan payments, insurance. These are contractual, predictable, and largely non-negotiable.

- Variable Necessities: Groceries, utilities, gas. Essential, but flexible month to month.

- Discretionary Spending: Dining out, streaming services, shopping, entertainment. This is where habits quietly drain momentum.

Here’s the contrarian take: most people obsess over cutting lattes while ignoring bigger structural issues. Yes, daily coffee adds up. But trimming $40 in caffeine won’t fix a $400 car payment that’s stretching your income thin. Focus on impact, not optics.

As you scan your spending report, look for patterns. Subscription creep is common—$9.99 here, $14.99 there, until you’re funding five platforms you barely use (no judgment, we’ve all rage-subscribed after a cliffhanger finale). Impulse online purchases and convenience food runs also spike more than people expect.

This is your “Aha!” moment: which category surprises you? That emotional reaction is data.

Some argue strict categorization feels restrictive. But structure creates freedom. A zero based budgeting guide pushes you to assign every dollar a job, exposing waste with uncomfortable precision.

Pro tip: Sort discretionary spending from highest to lowest. The top three items usually reveal 80% of the problem (a nod to the Pareto Principle, Harvard Business Review).

Ultimately, categorizing isn’t about guilt. It’s about control. And control is where real financial insight begins.

Step 3: The Action Plan – Implementing High-Impact Cost-Saving Techniques

You’ve reviewed the numbers. Now it’s time to act. This is where intention turns into traction—the sound of expenses tightening, the quiet relief of control returning.

Technique 1: The “Needs vs. Wants” Audit

A need is essential for survival or work (rent, utilities, groceries). A want improves comfort or enjoyment (streaming services, takeout, upgraded gadgets).

Go line by line through your bank statement. Ask:

- Is this essential?

- Can it be reduced?

- Can it disappear entirely?

Some argue small purchases don’t matter. But research shows habitual discretionary spending compounds over time (Federal Reserve, 2023). That daily $6 latte? It smells amazing—but it’s $2,190 a year.

Technique 2: The Subscription Purge

Open your statements and highlight every recurring charge. Yes, even the $4.99 ones hiding quietly.

- Cancel what you don’t use.

- Downgrade what you barely use.

- Set calendar reminders before free trials renew.

(If you forgot you had it, you probably don’t need it.)

Technique 3: The Grocery Game Plan

Groceries are tactile—the hum of refrigerators, the smell of fresh bread. Go in with armor: a list.

- Meal plan weekly.

- Shop your pantry first.

- Switch from brand loyalty to price comparison.

Studies suggest meal planning can cut food waste and reduce spending by 15–20% (USDA). Pro tip: never shop hungry.

Technique 4: Negotiate Fixed Bills

Call providers and say: “I’ve been a loyal customer. Are there any promotions or loyalty discounts available?”

Many hesitate, assuming rates are fixed. They aren’t. Competition drives flexibility.

Build Around a Budgeting Model

Use the 50/30/20 rule:

- 50% needs

- 30% wants

- 20% savings

If you want structure, follow a zero based budgeting guide and assign every dollar a job.

Still unsure about tools? Compare approaches here: digital vs manual budgeting tools which works better.

This is the moment your finances stop feeling chaotic—and start feeling intentional.

Step 4: Automate and Adjust – Making Your Budget Work for You

At this stage, your goal is simple: make your budget sustainable and nearly effortless. That starts with automation.

First, set up automatic savings. The “pay yourself first” principle means money moves to savings the moment your paycheck lands—not after you’ve spent what’s left. Schedule a recurring transfer to a high-yield savings account on payday. According to behavioral finance research from Duke University, automating decisions increases follow-through because it removes willpower from the equation.

Next, automate bill payments for fixed expenses like rent, insurance, and utilities. Auto-pay reduces late fees (which average $32 per missed payment, per CFPB data) and lowers mental load.

Finally, schedule a 15-minute monthly check-in. A budget is a living document. Review upcoming expenses, income changes, and adjustments using a zero based budgeting guide. Small tweaks each month prevent major setbacks later (think of it as routine maintenance for your money).

Take Control of Your Financial Future Today

You came here looking for a clear path to take control of your money — and now you have it. With this four-step plan and the zero based budgeting guide, you’re equipped to build a budget from scratch and cut costs with purpose. Financial uncertainty is stressful, but structure replaces stress with clarity. When you base decisions on your real numbers and commit to small, consistent actions, the savings compound faster than you think.

Don’t let another month slip by feeling behind. Start today — choose your tracking tool and log your first expense. Take action now and turn clarity into lasting financial growth.