Building wealth isn’t just about picking the right investments—it’s about keeping them aligned with your goals as markets shift. This portfolio rebalancing guide delivers a clear, actionable framework to help you balance risk and reward, even during periods of volatility. Many investors unknowingly drift from their original strategy, exposing themselves to unnecessary losses or missed growth opportunities. Grounded in time-tested financial principles used by seasoned experts, this guide walks you through not only the “what” and “why” of portfolio balancing, but the exact “how”—with step-by-step actions you can implement immediately to strengthen long-term performance.

What is Portfolio Balancing and Why Does It Matter?

Portfolio balancing—also called rebalancing—is the disciplined process of restoring your investments to a predetermined target allocation. In simple terms, asset allocation is your strategic blueprint (for example, 70% stocks and 30% bonds), while rebalancing is the routine maintenance that keeps that blueprint intact.

Over time, markets drift. If stocks surge, your 70/30 mix might quietly become 80/20. That shift increases risk, even if it feels like you’re winning. Rebalancing corrects this by trimming outperforming assets and adding to underperformers. In effect, it systematizes the classic advice to “sell high and buy low” (something investors say but rarely practice consistently).

Think of it like rotating your car’s tires. You’re not fixing what’s broken; you’re preventing uneven wear. Similarly, rebalancing protects long-term portfolio health by keeping risk exposure aligned with your goals.

Some argue rebalancing limits upside because you sell winners too soon. That’s fair—during bull markets, letting profits run can boost returns. However, research from Vanguard shows disciplined rebalancing reduces volatility without significantly sacrificing returns (Vanguard, 2020). Stability compounds quietly.

If you’re unsure about your allocation foundation, review stocks vs bonds finding the right portfolio mix.

Pro tip: Set calendar-based reviews annually or semiannually—emotion-free decisions outperform impulse moves.

For deeper tactics, consult a structured portfolio rebalancing guide before making adjustments.

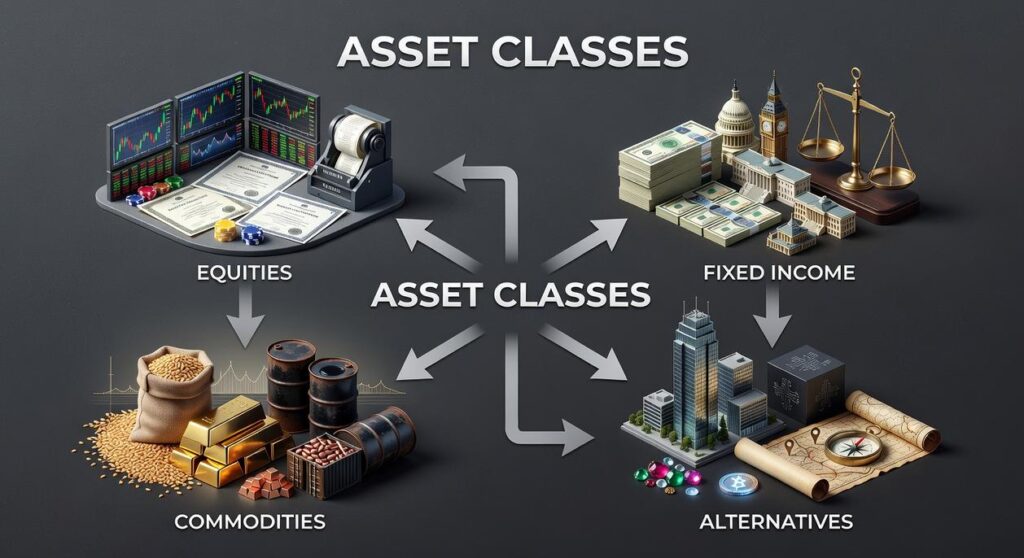

The Building Blocks: Key Asset Classes to Consider

A strong portfolio isn’t built on guesswork. It’s built on asset classes—groups of investments that behave similarly in the market. Each plays a distinct role, and decades of market data back that up.

Equities (Stocks): The Engine for Growth

Equities represent ownership in companies. Historically, U.S. stocks have returned about 10% annually over the long term (S&P Global). That growth, however, comes with volatility.

- Large-cap stocks (companies valued at $10B+) tend to offer stability. Think established brands like Apple—less explosive, but resilient.

- Small-cap stocks often deliver higher growth potential, though with sharper swings. According to Morningstar, small-caps have outperformed large-caps over certain multi-decade periods, albeit with higher risk.

- International stocks add geographic diversification, which can reduce overall portfolio volatility (MSCI research shows global diversification lowers single-country risk).

Fixed Income (Bonds): The Anchor for Stability

Bonds are loans you give to governments or corporations in exchange for interest payments. When stocks fell 37% in 2008, high-quality U.S. government bonds gained value (Bloomberg data). That cushioning effect matters.

- Government bonds: Lower risk, lower yield.

- Corporate bonds: Higher income, but more credit risk.

Cash and Equivalents: The Foundation of Liquidity

Cash provides flexibility. It covers short-term needs and acts as “dry powder” during downturns. Investors who held cash in early 2020 could deploy it during the COVID dip—when markets rebounded sharply within months.

Alternative Investments (Optional)

REITs and commodities offer diversification beyond stocks and bonds. REITs, for example, have historically provided competitive returns with income potential (Nareit data). However, they carry unique risks like interest-rate sensitivity.

Together, these building blocks form the basis of any portfolio rebalancing guide—balancing growth, stability, and opportunity with evidence on your side.

Your 4-Step Rebalancing Checklist

A few years ago, after a roaring bull market, I logged into my account and felt like a genius. Then I noticed my careful 60/40 mix had quietly morphed into 72/28. That was my wake-up call. Here’s the simple portfolio rebalancing guide I wish I’d followed sooner.

Step 1: Establish Your Target Allocation. Start by defining your ideal asset allocation—the percentage split between asset classes like stocks and bonds. Asset allocation simply means how you divide investments based on risk tolerance, time horizon, and goals. For example, someone saving for retirement in 30 years might choose 60% stocks and 40% bonds. In contrast, someone five years from retirement may prefer a more conservative tilt. Be honest about volatility; if market swings keep you up at night, adjust accordingly.

Step 2: Analyze Your Current Portfolio. Next, review your holdings and compare them to your target. Market momentum can push allocations off course. For instance, a strong equity rally might inflate stocks to 70%, leaving bonds underrepresented. This drift happens gradually, which is why regular check-ins matter.

Step 3: Identify What to Buy and Sell. Determine which assets are overweight and which are underweight. Overweight positions need trimming; underweight ones need reinforcement. Think of it as pruning a garden so everything grows evenly.

Step 4: Execute the Rebalance. Finally, either sell portions of overperforming assets to buy underperformers, or direct new contributions exclusively toward the underweight categories until balance is restored. Prefer second method when possible—it feels painful.

Finding Your Rebalancing Rhythm: Calendar vs. Threshold

The CALENDAR method means rebalancing on a fixed schedule—quarterly, semi annually, or annually. It is simple and disciplined, like autopay for your portfolio (set it and forget it). But critics argue it can ignore sharp market swings between dates.

The THRESHOLD method triggers trades only when an asset class drifts 5% or 10% from target. It is more responsive, yet demands closer monitoring.

A vs B? Structure versus sensitivity. The best choice is the one you will follow consistently, as any solid portfolio rebalancing guide will stress. Consistency beats perfection over time always.

From Theory to Action: Building a Stronger Financial Future

You came here to move from theory to confident action—and now you have the tools to do exactly that. An unbalanced portfolio leaves you exposed to market swings, second‑guessing decisions, and reacting out of fear. A disciplined approach puts you back in control.

By consistently applying the principles inside this portfolio rebalancing guide, you replace emotion with structure and build a resilient foundation for long‑term wealth.

Now take the next step: set aside 15 minutes this week to review your asset allocation and lock in a rebalancing schedule. Small, consistent actions today create financial strength tomorrow—start now.